Ether is Undervalued: Ethereum 2.0 Upgrades Project a 25k Price Target

Applying Stock to Flow Modeling To Ether

Written by Dheepan Ramanan & Ivan Kopas

With a total market cap of $2 trillion, cryptocurrencies are becoming widely accepted as mainstream financial instruments. However, there is still a lack of media coverage about major cryptocurrency networks and how they can be valued. As a consequence, Ethereum, the second largest cryptocurrency, does not receive nearly as much attention as Bitcoin today. This is despite the truly disruptive potential of the Ethereum network. In our view, this capacity dramatically eclipses the capabilities of the original cryptocurrency.

Unlike Bitcoin, the Ethereum network not only functions as a currency, but also as a decentralized computing network which has the potential to change how we conduct finance, how we build and deploy web applications, and even how we exchange and validate art.

Despite this technological potential, Ethereum, and it’s currency Ether (ETH), have traditionally had inferior monetary characteristics to Bitcoin. Ether held higher rates of inflation and there were more technological uncertainties of the final build of the network. With the advent of Ethereum 2.0 in late 2021/2022, we believe these concerns will be addressed. We believe that the magnitude of the impending monetary supply shock is not understood by the market and has the potential to lengthen the crypto bull market into 2022.

Utilizing stock-to-flow (s2f) modeling developed for Bitcoin we see a year-end target of $5k per ETH, with a long term bull case of $25k per ETH.

Background of Ethereum

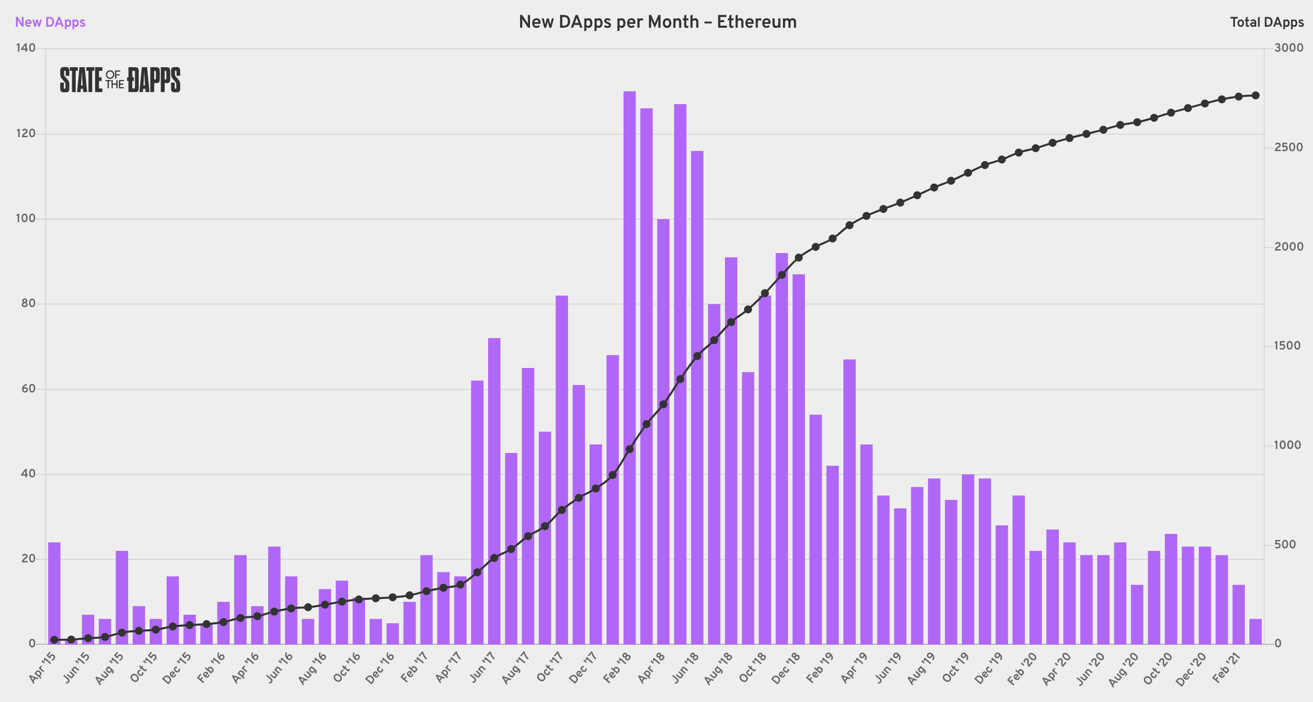

Ethereum is a community-run open-sourced project, originally proposed in 2013 by Vitalik Buterin and officially released in 2015. Ethereum is a blockchain network like Bitcoin, but envisioned with a different utility. Unlike Bitcoin, which is generally viewed as “digital gold” due to its store-of-value property, Ethereum was created to be a decentralized blockchain platform. Ethereum has been used to host Decentralized Finance protocols (DeFi), Decentralized Applications (dApps), Initial Coin Offerings (ICOs), and Nonfungible tokens (NFTs). Ethereum network’s native currency, Ether (ETH), where each ETH consists of 1018 wei units, is the fuel of the network, pumping “life” into nearly 3000 dApps. In his TED talk, back in 2007, Jeff Bezos compared the Internet to the early days of electricity, portraying its enormous potential to power our digital future. In a similar fashion, we can now view ETH as the “electricity” that will be powering the decentralized Ethereum network, fueling its growth and keeping the lights on.

The Double-Edged Sword of Ethereum Adoption

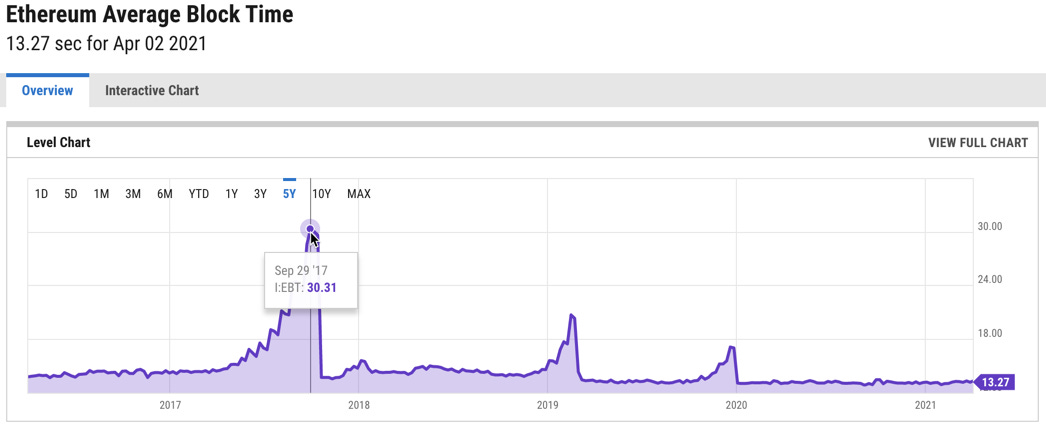

Ethereum is by far the most popular blockchain platform for dApps and smart contracts. However, with this adoption creates scalability challenges for the network. Perhaps the best example dates back to 2017, when the CryptoKitties dApp saw such a massive influx of users that the Ethereum blockchain got clogged with a backlog of over 30,000 transactions, resulting in a massive spike of the average daily block processing time.

The solution to the clogged up blockchain network involved raising the transaction fees, which discouraged the CryptoKitties users from generating new transactions at such a high rate, ultimately leading to the clearing of the transaction backlog. This loop actually dampens network growth, as transaction capacity limits the scale and number of applications that can run on the Ethereum network.

The Path to Serenity: Proof of Stake

Part of Ethereum’s scalability challenge lies in the Proof-of-Work (PoW) mechanism that the entire Ethereum ecosystem relies on for validating transactions captured on the blockchain. The PoW mechanism (borrowed from Bitcoin), is compute-heavy and costly in terms of utilized electricity. In PoW each transaction within each block must be independently verified by solving a cryptographic “puzzle”. This creates limited throughput in the network, resulting in higher amounts of fees.

However, as part of ETH 2.0, the second generation of Ethereum, the blockchain network will transition from PoW to Proof of Stake (PoS) consensus mechanism. In the PoW system, everyone attempts to solve the “puzzle” and the entity with the largest compute power typically gets to solve it first and write the block to the blockchain. In contrast, in the PoS system the entity that puts the largest number of coins at “stake” (temporarily stored away in a highly restricted wallet that freezes the coins), gets entered into a randomized drawing raffle in order to get the opportunity to write the block. The “winner” then writes the block to the blockchain and gets rewarded by receiving the amount of ETH of the transaction fee.

Following are some of the key benefits of the PoS consensus mechanism:

Fair play - encourages all entities to “play by the rules” as a bad actor would run into a risk of losing all of their staked coins.

Decentralization - unlike in the PoW system, where several big players that can afford the largest tech stack of specialized hardware (ASICs) would be able to control the process of writing the blocks to the blockchain, in PoS system the randomization factor combined with the volume of staked coins ensures that the control of writing the blocks to the blockchain is decentralized.

Lower electricity consumption - due to the high computational power requirement of PoW, the electricity cost tends to run very high. However, in the PoS system, the removal of the need for high computational power eliminates the need for high electricity usage.

ETH 2.0 features other changes including splitting up the blockchain into smaller pieces (sharding), all of which will lead to much higher throughput and lower fees on the network.

ETH 2.0: Turning Ether Into A Reserve Asset?

The introduction of ETH 2.0 not only intends to scale the network to alleviate congestion, but also to introduce technical changes (EIP-1559) that realign the economic incentives of the Ethereum network. Today, the token of Ethereum (Ether) is inflationary and the supply of currency is not programmatically scheduled, but linked to how easily miners can mine new currency in a PoW system. Miners in the Ethereum network get paid through transaction costs paid by users of the network as well as block rewards which generate Ether (reward for solving proof of work, providing security to the network). To transact on the network, the users bid in an auction style manner to get their transactions through the network. These factors incentivize high fees and network congestion as users bid up transaction prices to get faster execution and miners benefit from higher transaction fees. In addition, these incentives align with lower mining difficulty and thus higher amounts of Ether inflation. Greater supply keeps the price of Ether lower, managing the escalating transaction costs. With this structure in place, the Ether monetary base grew very quickly, doubling the total money supply in 5 years.

Ethereum 2.0 changes this system so that growth in the network rewards individuals who hold Ether. In 2.0, miners are replaced with “validators”, individuals with at least 32 Ether who validate the transactions on the network using proof-of-stake. Compared to traditional finance, this concept is analogous to a convertible bond. Validators are paid a percentage yield in Ether (like a bond coupon), and after two years validators receive back their principle in converted Ether, which theoretically appreciates against fiat currency (like a bond which converts into stock). Like companies who issue bonds, Ether incentivizes early adopters with a higher bond yield (currently at 10% APR). This yield declines to roughly 2% after enough validators are added to the network. This yield is the only new Ether added to supply, which caps total inflation.

In addition to this “convertible bond”, Ethereum 2.0 also adds elements analogous to dividends and stock-buybacks. In the new system, all transactions on the Ethereum network have a base transaction fee and an optional tip. The base fee is paid to the network and this Ether is removed from the circulating supply. In traditional finance this would be similar to a stock buyback program where 100% of all free cash flow reduces supply of stock. In addition, validators receive “tips” to process certain transactions quicker, much like a special dividend returns excess business cash to stock-holders.

Today, Ethereum grows its network by over 100,000 addresses a day and already has transaction fees over 4x of Bitcoin at one fourth of the market cap. If user growth is maintained, even at lower average fees, the volume of Ether burned in transactions could produce a deflationary response in total supply. As the utility of the Ethereum network grows (more dApps, DeFi protocols, NFTs, etc) the value of Ether, the principal currency of the network, should naturally rise.

Stock To Flow: Ether Prediction Targets

As part of our investigative efforts to price Ether, we recreated the popular Bitcoin models from PlanB. PlanB popularized “stock to flow” regression models which use a single dependent variable (stock-to-flow) fitted against price or market cap. Stock-to-flow is calculated as current supply/(current supply-prior year supply). PlanB found that there was strong evidence that this stock-to-flow predicted Bitcoin price, and secondly that this variable followed a power law. This meant that increases in stock to flow resulted in exponential increases in asset price. We tested both the traditional stock-to-flow model as well as the stock-to-flow cross-asset model, fitting the models on both Bitcoin and Ethereum data. We plan to open-source this code later this month.

Overall, we found that previous Ether price data like Bitcoin rose as Ether’s stock-to-flow value improved. The statistical error metrics did not show a strong relationship like we saw for Bitcoin. This is likely because the Bitcoin halving cycle and subsequent increases in price are what drive Ether’s price to date. Ether has so far acted as a riskier crypto asset with more volatility than Bitcoin. However, unlike the prior halving cycle where Ethereum was brand new, today Ethereum outpaces Bitcoin in transaction fees, open source developers, and decentralized applications. With the advent of Ether 2.0 which establishes Ether as the principal reserve asset of a large crypto network independent of Bitcoin, we see the stock-to-flow model as more applicable to evaluate Ether than in prior cycles.

We observed that the statistical performance of the models stayed level or improved with the addition of Ether data points (out-of-sample and in-sample improvements with the cross-asset model, and out-of-sample improvement with the generic stock-to-flow model). For context, we mapped Bitcoin’s previous halving cycle (6/2014-3/2019), which featured very similar stock-to-flow values to Ether presently.

If Ether’s behavior reacted the same as Bitcoin’s historical stock-to-flow, $5,000 per ETH would represent fair value.

When we fit Ether stock-to-flow values and Bitcoin’s stock-to-flow values, the models became more conservative, but were still largely predictive. The cross-asset model assigns a more conservative target to lower stock-to-flow values, whereas the regular stock-to-flow model assigns a higher multiple.

Given that the statistical results for out of sample results for the regular stock to flow model were stronger, it is possible that this model is better at predicting earlier stage crypto price movements. As a result, in the short term (3 to 6 months), we expect the price of Ether to jump to increase to a minimum of $2,500.

A Second Crypto-Supply Shock?

The long term implications are much more dramatic. Although the prior crypto bull markets rose and declined with the Bitcoin halving cycle, ETH 2.0 is not discussed as an equally disruptive supply shock to the crypto market. With the improvements to the scalability of the network, and the new economic structure of Ether, we expect new supply of Ether to decline. Given that the launch of ETH 2.0 will occur towards the end of this year or early 2022, the crypto market will see a secondary supply crunch to the second largest cryptocurrency a full 18 months after the Bitcoin halving. This has the potential to lengthen this current crypto bull market beyond previous halving events.

In this scenario, today’s Ether price is extremely cheap. Long term the new supply of Ether is likely deflationary, but even reaching Bitcoin’s current level of inflation of 2% creates a 10x opportunity. At that level, Ether’s higher stock-to-flow ratio predicts a multi-trillion market cap. At a conservative 2% annual inflation, our expected Ether price by 2024 is between 25k-32k, a 12x return from today’s Ether price.

Disclosure: the authors are long BTC and ETH

Let say the current S2F of ETH is 24, according to PlanB's S2FX model, the expected market value is e^12.7598 * 24^4.1167 = 167B, divided by the 116M supply gives the expected price of $1442. So, the current price has over reflected?

Hi Dheepan - how do you explain for the contradiction of views/analysis of S2F on Ethereum when PlanB (whose idea this is - S2F) says that it is not applicable to Ethereum as Eth is not scarce, and S2F oy applies to things that are scarce.

Thanks in advance for your response, really interested in your views on this.